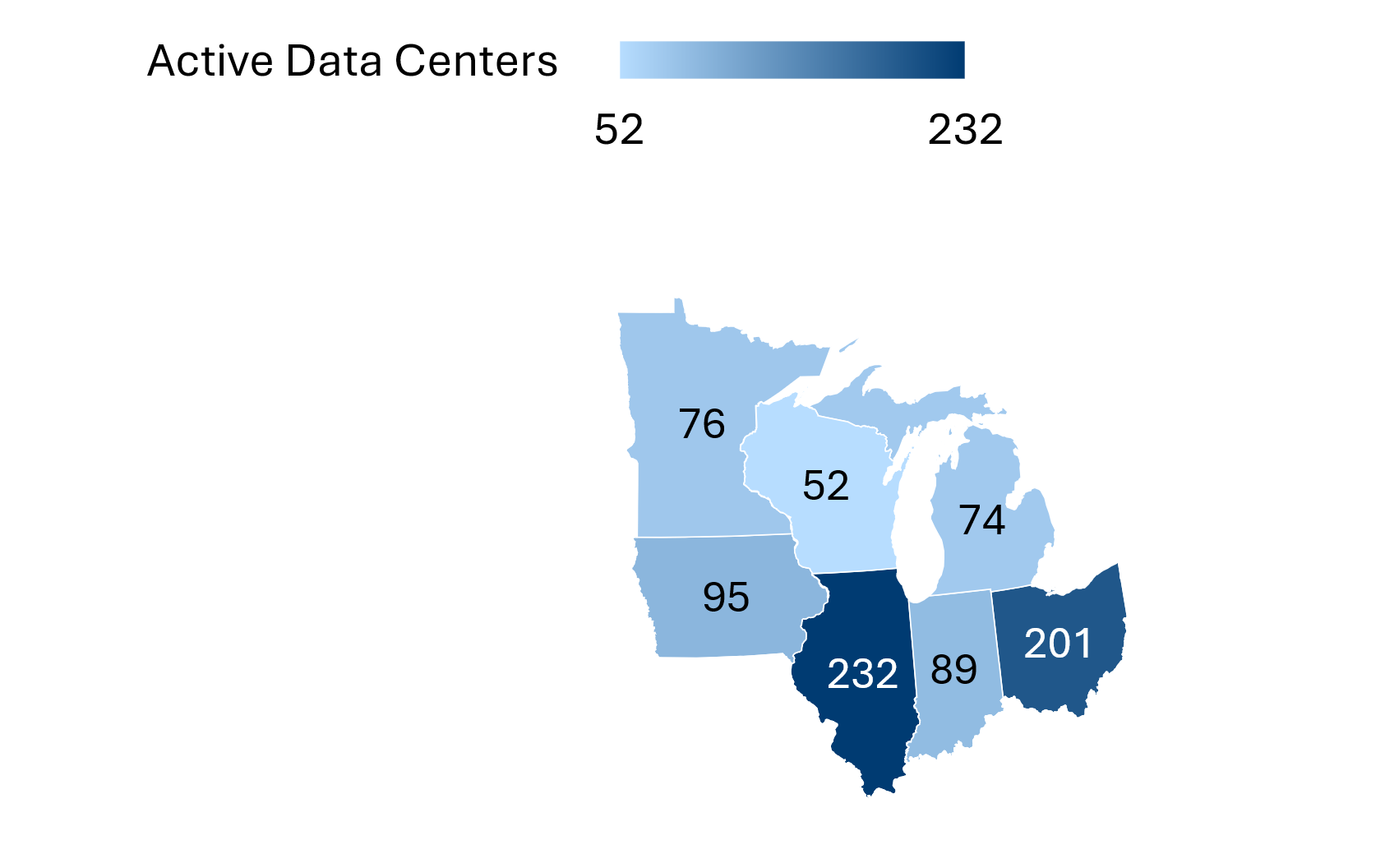

As focused on in our last digest, a massive data center buildout is currently underway nationwide. One region experiencing high growth is the Midwest, particularly in Illinois around Chicago and central Ohio (Figure 1). While states such as California and Virginia lead the country in the number of data centers, the Midwest is emerging as an efficient region to build out new power capacity and tap the resources necessary to enable data centers. Early in data center development, most were clustered in hot-spot regions, like Northern California and Northern Virginia. Now, the Midwest is part of the long tail of states where development is growing. That growth is already reshaping the resource economics of the region.

Figure 1: Active Data Centers in Midwestern States

The Midwest is defined in this digest encapsulates the seven-state geography of Illinois, Indiana, Iowa, Michigan, Minnesota, Ohio, and Wisconsin.

Source: Data Center Map.

All four of the big tech data center builders—Amazon, Google, Meta, and Microsoft—are active in the region and have been supporting the development of data center growth since the 2000s. While most of the existing data centers in the region use relatively little electricity—under or about ten megawatts (MW)—recent estimates put the development potential of the region as high as five gigawatts (GW). For comparison, that power draw would require the generation capacity of two-and-a-half Hoover Dams.

How to meet that power demand is a point of contention nationwide, and that is exemplified by two proposed projects in the Midwest. An Inside Climate News article exemplifies this contention, contrasting renewables– and demand response-powered Google and DTE Energy data center sited in Michigan and a natural gas-powered data center funded by two Japanese companies in Ohio. Regardless, the buildout of data centers is also constrained by the availability of grid capacity, which is a frequent topic of concern for stakeholders across industries.

Some local communities where data centers have been proposed are fighting these proposals. One $500 million Metrobloks facility proposed in Indianapolis, Indiana, has met with significant community disapproval over the past six months. Concerns over pollution, electricity affordability, and a lack of local job creation form the baseline of the majority Black community’s complaints. On the other hand, the project will provide $10 million in property tax revenue for the city annually, and Metrobloks committed $2.5 million for the construction of infrastructure and affordable housing in the area. Another $800 million data center project in Michigan City, Indiana, that is already under construction, continues to face community backlash because of concerns over air pollution from its diesel generators, and activists and communities in Wisconsin are also fighting data center developments because of concerns that their high energy demand could increase residential energy bills.

State legislatures and regulators are taking notice. In Michigan, a bill to pass a moratorium on new data centers is working its way through the legislature. Also in the state, the Michigan Public Service Commission voted in late March to deny a reconsideration of a planned 1.4 GW data center. In Illinois, the state’s Commerce Commission approved new terms with data centers after a recorded rise in electricity costs and will open an investigation into further residential consumer protections. In Iowa, however, a proposed bill would provide a state sales tax exemption to data centers during construction and expansion, meant to attract greater investment in the state. Utilities across the region are eager to serve new loads but are imposing new requirements to balance impacts on all ratepayers. In a recent rate case in Ohio, AEP Ohio added a minimum monthly electricity charge for new data centers, joining an existing utility data center tariff.

Per our last digest, states are in a discovery phase when it comes to how to approach regulating data centers, and this is reflected in the Midwest. Balancing economic development with potential environmental harms is a central tension in large infrastructure projects. States must work quickly to understand and ameliorate this novel regulatory landscape, especially as the average domestic data center is forecasted to rise from 40 MW to 60 MW by 2028.