Data center growth in the United States has skyrocketed in the past couple of years. Data Center Map currently logs more than 4,000 data centers nationwide, with at least one in every state. Most of these data centers are near major metropolitan areas. Prime destinations include Northern Virginia and Northern California, with Illinois, New Jersey, and New York climbing the list of ideal data center destinations, likely driven by the availability of power and internet infrastructure. All those data centers require many a watt to operate. Amid concerns of rising electricity prices, how are states attempting to ensure that data centers do not squeeze power supply or water resources?

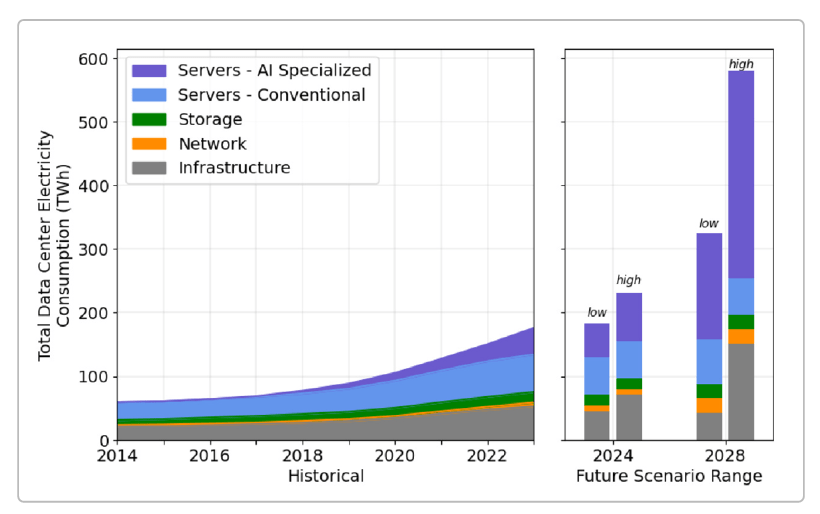

First, it is important to understand how much electricity data centers use. In 2010, data center electricity demand represented about two percent of national electricity sales and remained steady throughout the decade, between 60 and 70 terawatt hours (TWh). Gains in efficiency held down any potential increase in consumption. However, since 2017, demand has steadily increased. In 2023, domestic data centers demanded 176 TWh, or about 4.4 percent of national electricity sales. Now, a U.S. Department of Energy study estimates that electricity demand from data centers could triple by 2028 and require up to 12 percent of U.S. electricity demand (Figure 1). The International Energy Agency has projected that through 2030, about half of new demand in the United States will stem from data centers.

Figure 1: Annual domestic data center energy use (2014-2022) and projected demand (2024 and 2028)

Source: Yale Clean Energy Forum

Facing this anticipated load growth, states have begun to seriously consider the impacts that data center demand may have on their grid and transmission systems, and how they may affect electricity prices for commercial, industrial, and residential customers. According to WilmerHale, an American multinational law firm, more than 200 data center-related bills were introduced in 2025, with at least one in every state. More than 40 of these bills were eventually enacted. Many of these bills aim to rein in how much electricity and water data centers can draw from public supplies, in addition to siting requirements, labor standards, and security precautions.

There were 55 bills introduced in U.S. states between January 2024 and February 2026 that pertained to data center energy usage, based on analysis of data from Legiscan. These bills were introduced in 20 states, with the highest number of bills in New York and Virginia.

Some states are requiring data centers to benchmark their performance. Illinois’ SB2181 seeks to create data center reporting standards for energy and water use. In addition to annually reporting a facility’s energy and water consumption to the Illinois Power Agency, the bill also outlines tight data confidentiality on the information reported. However, it does require the Illinois Power Agency to create and submit a study and report on how data centers are impacting rate payers in the state. The bill was introduced in February 2025 and as of March 13th, 2026 sits in the Senate’s AI and Social media committee.

Others are going one step farther in attempting to lower resource consumption. One such bill is SB1196 out of Virginia, which would have provided a financial incentive for data center operators to meet certain state energy efficiency standards. In order for a data center to qualify for sales and use tax exemptions, the facility would have been required to demonstrate certain power usage effectiveness scores and to acquire 90 percent of its electricity from renewable energy sources. Introduced in January 2026, the bill died in the Senate Finance and Appropriations Committee.

Some states, perhaps recognizing they need more time or information to write effective regulation, are attempting to pass moratoriums on the creation of new data centers powering AI. Michigan’s HB5595 (in the Committee on Government Operations), New York’s S09144 (in the Senate’s Environmental Conservation Committee), and Vermont’s S.205 (in the Senate Finance Committee) are three such active examples from this legislative cycle.

This is by no means a comprehensive summary, but even so, the disparate nature of these approaches reveals that states have not settled on a common approach. The growth in data center construction is very new. Each state is trying to balance the economic development that comes with new infrastructure against the potential for resource restrictions and price increases. As the data center boom continues, states will learn more about what works and what doesn’t, and a clearer picture of how to manage this rapid demand growth will emerge.