The residential and commercial building landscape features a diversity of space heating, cooling, and water heating equipment. These technologies vary in terms of the fuels they draw on and their efficiency, with electric heat pumps and heat pump water heaters leading the way.

Space heating, cooling, and water heating powered by fossil fuels together make up about 13 percent of domestic emissions arising from commercial and residential buildings. As such, tracking the relative market shares of electric versus gas appliances and heat pumps versus furnaces or A/Cs helps illuminate how and whether federal and state programs and incentives, as well as the power of the market, are encouraging fuel switching or upgrading to more efficient, cleaner building technologies.

The Appliance Shipments dashboard on Buildings Hub visualizes monthly shipment numbers for space heating, cooling, and water heating appliances for 2012 through 2023. Data is publicly provided by the Air-Conditioning, Heating, and Refrigeration Institute (AHRI), the trade association representing commercial and residential HVAC and water heating manufacturers that produce over 90 percent of this equipment that is sold in North America.

AHRI releases data monthly, with a two-month lag for internal collection and compilation. Once the data is released, the Buildings Hub team inputs and surfaces it on the Appliance Shipments dashboard to provide as recent a picture as is available of the space and water heating and cooling market. Specifically, Buildings Hub collects data for the following technologies: Gas Warm Air Furnaces, Oil Warm Air Furnaces, Residential Gas Automatic Storage Water Heaters, Residential Electric Automatic Storage Water Heaters, Commercial Gas Storage Water Heaters, Commercial Electric Storage Water Heaters, Unitary Air Conditioning, and Unitary Heat Pumps.

On the dashboard and in this data story, appliance shipments between manufacturers and distributors are used as a proxy for sales, as both are indicators of demand. Note also that this data encapsulates shipments across North America, not just in the United States.

Space Heating

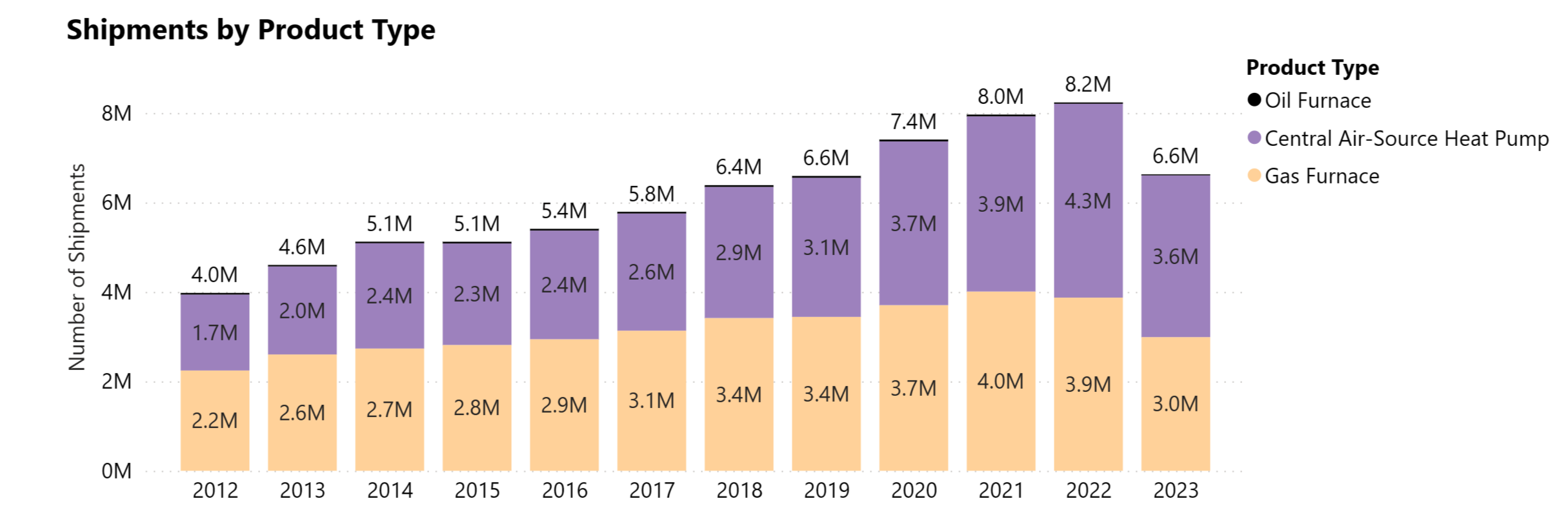

The space heating AHRI shipment dashboard differentiates between three product types: oil furnaces, gas furnaces, and central air-source heat pumps. In 2023, heat pumps outsold gas furnaces for the second year in a row, at about 3.6 million units compared to about 3 million units (Figure 1). Note that these figures include both residential and commercial appliance shipments.

Figure 1: Space Heating Equipment Shipments by Product Type Over Time

Source: Atlas Buildings Hub, Appliance Shipments dashboard

Since 2012, total shipments of space heating equipment have steadily increased, with 2023 being a notable exception. In 2012, about four million space heating products were shipped, rising steadily to 8.2 million in 2022. 2023 saw about a 20 percent decrease in total product shipments to about 6.6 million. Oil furnaces have seen their small market share of shipments decrease over time, with about 22,600 sold in 2023.

An article by Canary Media pointed to inflation, high interest rates, and supply chain bottlenecks which limited consumer spending and thus interest in purchasing new space heating equipment. Nevertheless, this slowdown in total sales did not stop mounting changes in market shares among technologies (Figure 2).

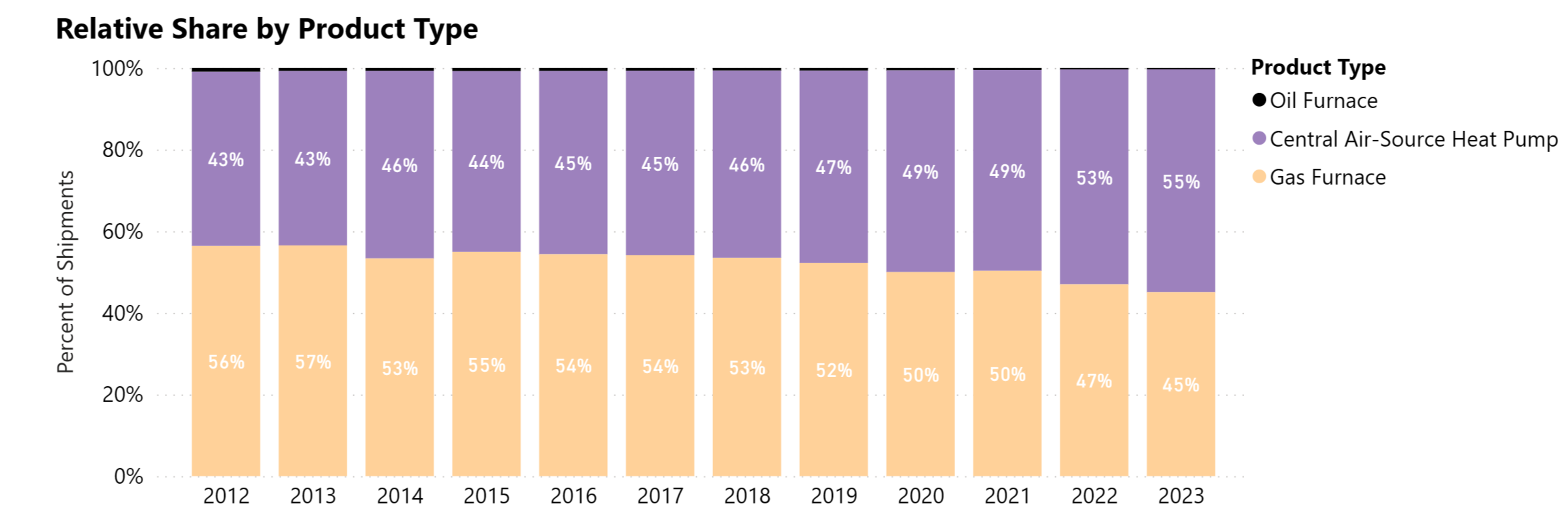

Figure 2: Space Heating Equipment Relative Market Shares by Product Type Over Time

Source: Atlas Buildings Hub, Appliance Shipments dashboard

Heat pumps have made consistent market share gains over the past ten years. Growth was particularly stark in 2022 with a four percentage point market share increase from 2021. While this jump aligns with the passages of the Infrastructure Investment and Jobs Act (IIJA) in November 2021 and the Inflation Reduction Act (IRA) in August 2022, the federal heat pump-related incentive programs have yet to be launched.

Research released by the National Renewable Energy Lab in March 2024 found that a majority of households would save money on space heating if they installed a heat pump (specifically, between 62 and 95 percent depending on the selected heat pump’s efficiency). This analysis does not take into account the cost savings a household would gain if leveraging federal or state incentives. As a result, further increases in shipments as well as pocketbook savings — more significant than those achieved between 2012 and 2019 — can be expected once the federal Home Energy Rebate Programs are deployed nationwide.

Cooling

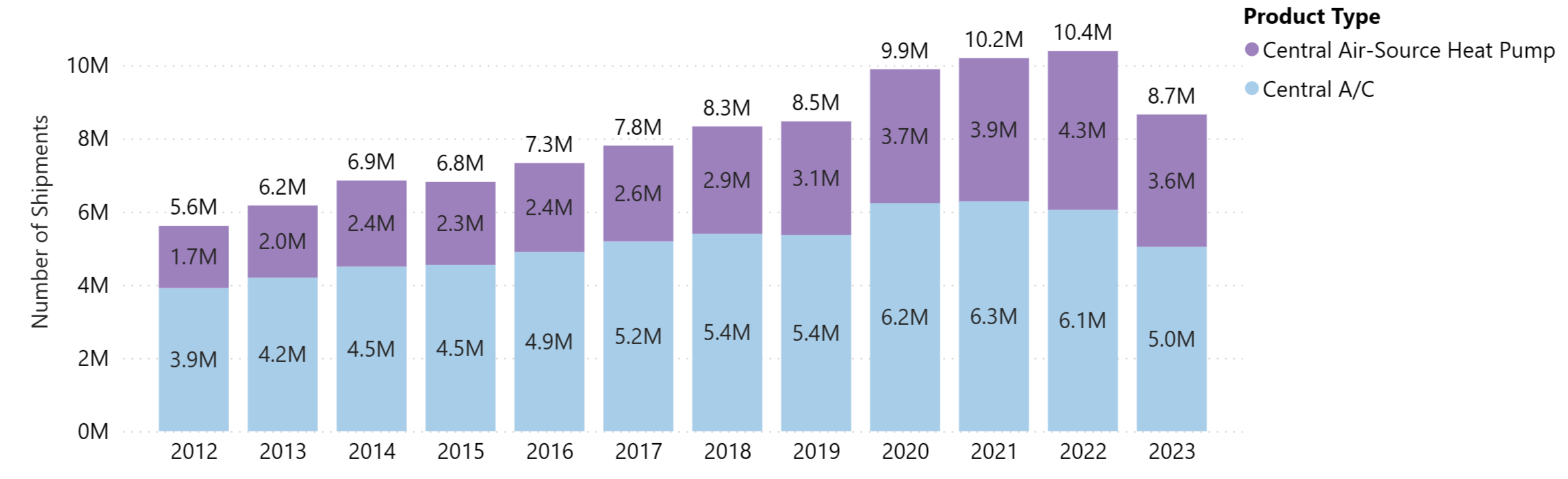

The cooling section of the Appliance Shipments dashboard examines shipments of central air-source heat pumps and central air conditioning systems. All of these figures include both residential and commercial appliance shipments.

Over the past ten years, the raw number of cooling products shipped has steadily increased, again apart from in 2023 (Figure 3). Similar to heating equipment, this drop-off can also be explained by inflation, high interest rates, and supply chain bottlenecks.

Figure 3: Cooling Equipment Shipments by Product Type Over Time

Source: Atlas Buildings Hub, Appliance Shipments dashboard

The number of cooling equipment shipments is and historically has been higher than the number of heating equipment shipments. In 2012, cooling equipment shipments were 29 percent higher than heat equipment shipments, while in 2022 and 2023 they were 21 percent and 24 percent higher, respectively. The effective useful lifetime of a central air conditioner lies between 12 and 15 years; furnaces can last between 15 and 30 years depending on their fuel. Like air conditioners, Unlike air conditioners or furnaces, however, a heat pump can provide both heating and cooling from one device.

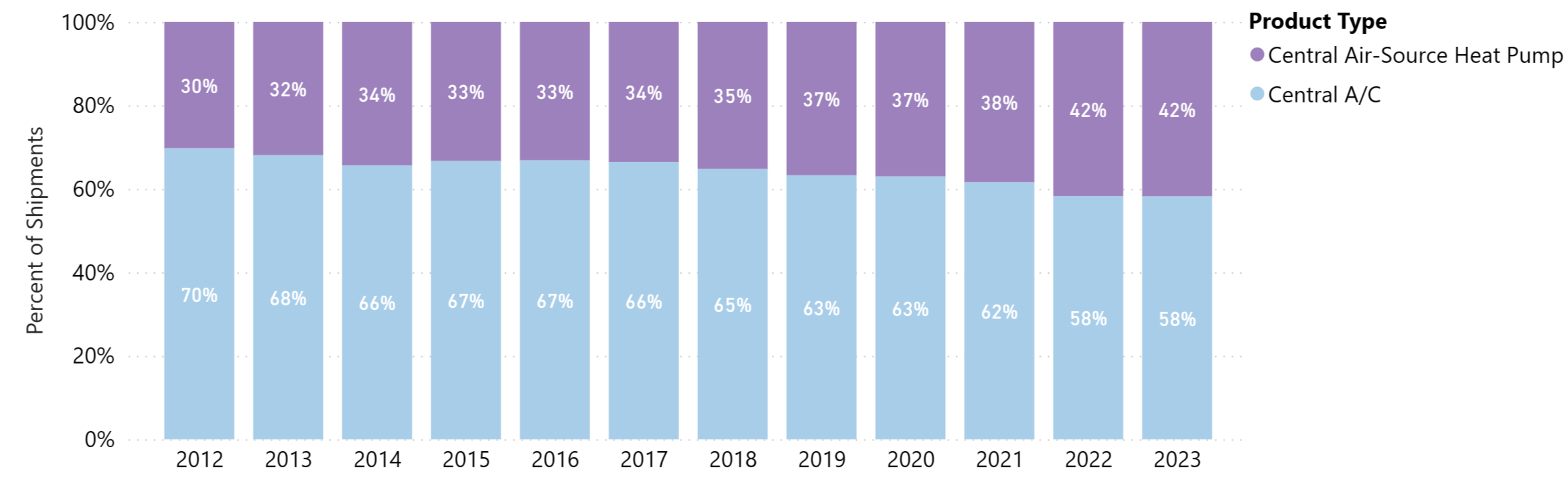

Like with heating equipment, heat pumps have also made gains in market share against air conditioners, although these gains are more incremental. Between 2012 and 2023, heat pumps rose from 30 to 42 percent of cooling equipment shipped, gaining 12 percent market share (Figure 4).

Figure 4: Cooling Equipment Relative Market Shares by Product Type Over Time

Source: Atlas Buildings Hub, Appliance Shipments dashboard

Between 2021 and 2022, central air-source heat pumps gained four percentage points of market share on central air conditioner shipments, similar to what occurred in the heating equipment market in the same year. While almost all air conditioners are powered with electricity, heat pumps are much more energy efficient. This saves the consumer money but is also a critical step in building decarbonization, given that energy use for cooling has more than tripled globally since 1990, with a 5 percent increase in energy use between 2021 and 2022. Moreover, total cooling energy consumption is projected to more than double by 2050. Heat pump installations will be a key tool to flatten that curve.

Water Heating

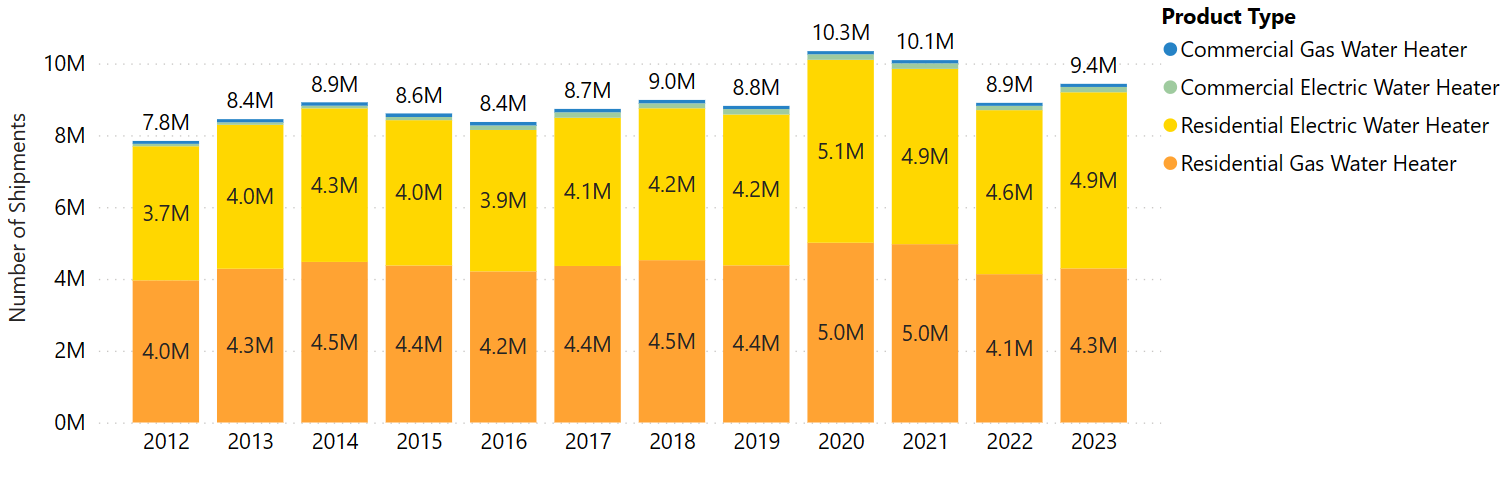

Total water heating equipment shipments do not appear to present a consistent trend over time (Figure 5). However, residential electric and gas water heaters have consistently represented the lion’s share of the water heating market.

Figure 5: Water Heating Equipment Shipments by Product Type Over Time

Source: Atlas Buildings Hub, Appliance Shipments dashboard

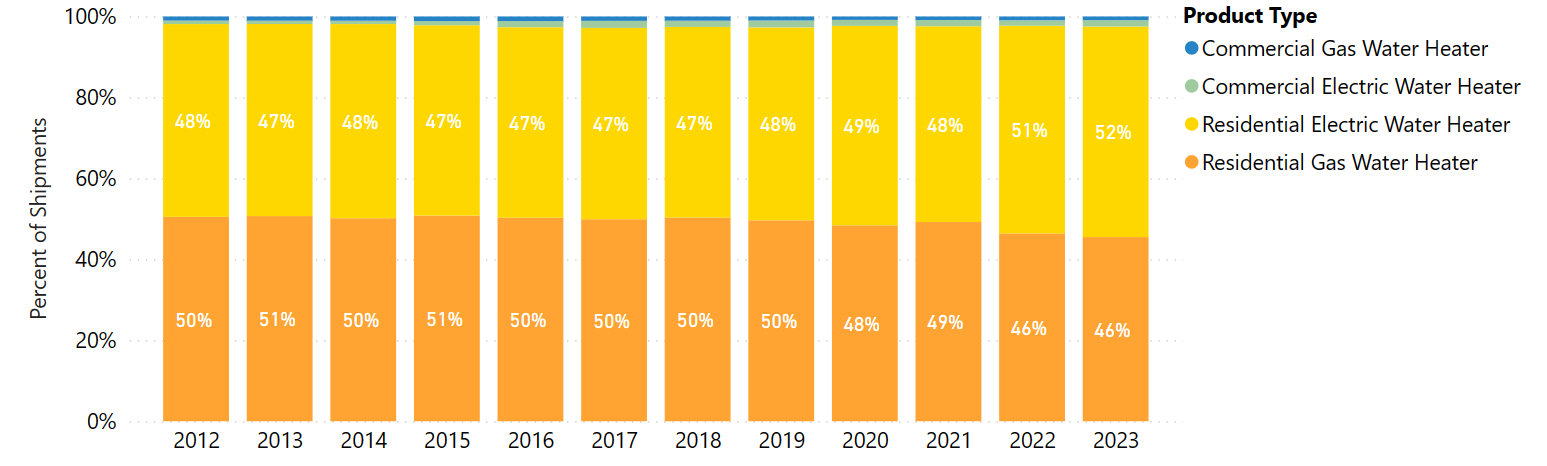

Market share information paints a clearer portrait of the popularity of these equipment types over time (Figure 6). Altogether, residential water heaters have represented 97 to 98 percent of the overall water heater equipment market between 2012 and 2023. Given their dominance of the market, discussion will focus on this market segment.

Figure 6: Water Heating Equipment Relative Market Shares by Product Type Over Time

Source: Atlas Buildings Hub, Appliance Shipments dashboard

Residential electric water heaters gained a four percentage point market share between 2012 and 2023. This relative gain is a third of the size of the percentage gains made by air-source heat pumps in space heating and cooling. Unfortunately, it is unclear what is driving this trend, particularly since granular data on water heaters by technology is not available.

Policies Push and Pull

While economic conditions pushed total appliance sales down in 2023, trends across the past decade indicate that consumer preference is shifting toward more energy efficient and often electric appliances.

National policy has only just begun to influence adoption of more energy efficient AHRI-tracked technologies, notably with the passages of the IIJA and IRA. The federal Home Energy Rebate programs are in the process of rolling out, with New Mexico being the first state to apply to both the Home Energy Rebate Programs: the Home Energy Performance-Based, Whole-House Rebates (HOMES) program and the High Efficiency, Electric Home Rebate Program (HEEHRA) on March 18, 2024. According to Department of Energy program manager Karen Zelmar, funds from the Home Energy Rebate programs should begin to hit states over the next three months. The addition of these federal incentives will only entice consumers to further adopt heat pumps and other electric, energy efficient appliances.