2025 was a tumultuous year for building electrification. A major shift in federal priorities meant progress on federally funded programs stalled. Electricity and piped gas prices continued to rise across the board, caused by a variety of factors including infrastructure upgrades and soaring demand. In particular, the cost of electricity rose faster than the rate of inflation, and politicians took aim at anything they could to try to stop or reverse the trend. Despite the headwinds, state and local governments continued to make progress on building electrification. Three trends stood out from the year that we want to highlight: heat pump sales continued apace, states continued to take advantage of federal funds to help building owners electrify, and more policymakers started taking a good look at geothermal energy to heat and cool networks of buildings.

Heat pumps increasingly outsold gas furnaces

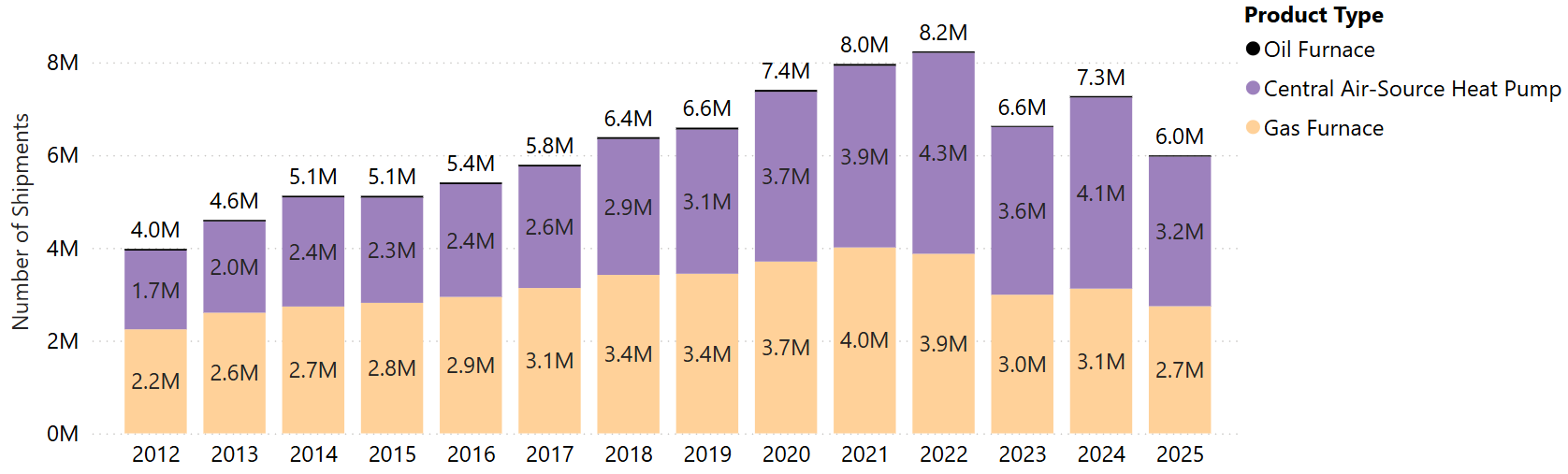

Each month, the Air Conditioning, Heating, and Refrigeration Institute (AHRI) publishes data on shipments of appliances for space heating, water heating, and cooling in the United States. In general, overall shipments of space heating, water heating, and cooling appliances increased from 2012 to the early 2020s until they started falling in 2023.

Shipments of all three types appear to be recovering, but until we have a full picture of 2025 (data releases from AHRI are on a three-month lag, so the data only currently go to October), it will be hard to know whether they have truly recovered. It is also worth noting that the data for space heating only include central air-source heat pumps, leaving out mini-splits and ground-source heat pumps, but as of the 2020 Residential Energy Consumption survey, only about one percent of households use mini-splits and another one percent use ground-source heat pumps compared to 12 percent with central air-source units, so the impact of the exclusion is small.

Shipments of space heaters were trending up for several years, doubling from four million in 2012 to 8.2 million in 2022 (Figure 1). Shipments fell in 2023 and did not recover as of October 2025. Heat pump sales, on the other hand, are continuing to grow as a percentage of space heating shipments. Even as overall space heater shipments fell from 8.2 million in 2022 to 6.6 million in 2023, the share of heat pumps in shipments rose from 53 percent to 55 percent and rose again in 2024 to 57 percent. From January to September 2025, the share of heat pumps was back down to 53 percent, but that may change when data for the final three months of the year are released by March 2026. Affordability is top of mind for many homeowners, and highly efficient heat pumps can help them save money. Plus, manufacturers are making heat pumps that work better in colder temperatures—one study of recent heat pump adopters in Massachusetts and New York found that customers were happy with their heating and cooling performance and they were able to save money on their bills.

Figure 1: Space Heating Equipment Shipments, 2012-Q3 2025

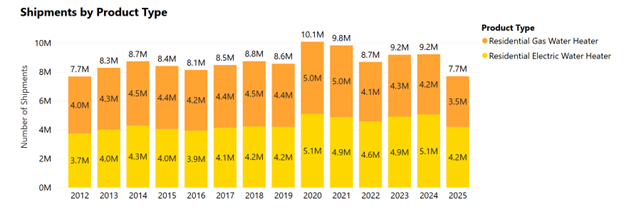

Shipments of water heaters have remained relatively stable since 2012, save for a slight jump in 2020 and 2021 and a decline after 2022 (Figure 2). Residential electric water heaters overtook their gas-fueled counterparts in 2022, and that trend continued in 2025. In the first three quarters of 2025, electric water heaters made up 54 percent of residential water heater sales with the remainder going to gas water heaters.

Electric water heaters are typically more efficient and cheaper to install than gas water heaters, which can help explain their increasing attractiveness when affordability is particularly salient.

Figure 2: Water Heater Shipments, 2012-Q3 2025

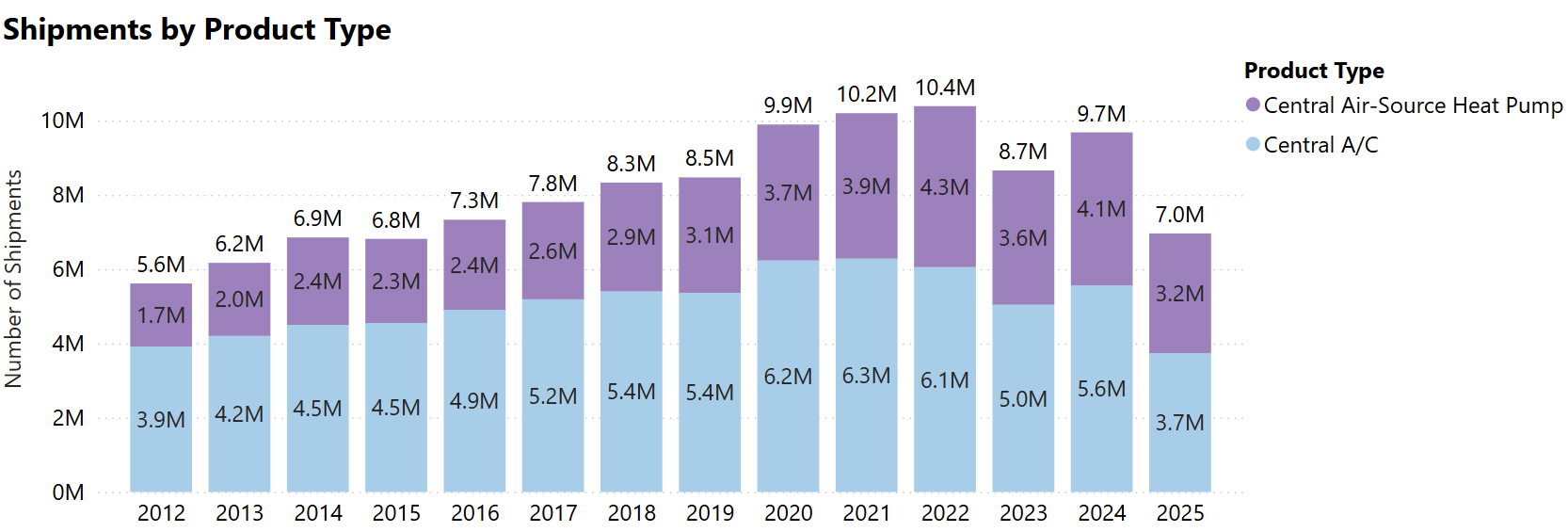

The pattern of shipments of cooling devices closely follows that of space heating, trending up until a brief dip in 2023 and what could be a recovery in 2025 (Figure 3). Much like space heating, shipments of cooling technologies are increasingly favoring heat pumps over traditional air conditioners, although heat pumps have not yet overtaken air conditioners for market share in cooling. Even as overall cooling shipments fell from 10.4 million in 2022 to 8.7 million in 2023, the share of heat pumps in the cooling market rose to 42 percent. From January to October 2025, the share of heat pumps in cooling technology sales continued to rise to 47 percent.

When considering cooling by itself, heat pumps and air conditioners are essentially the same product. However, the value proposition of a heat pump in heating and cooling is that it can provide both services in one device, as opposed to a separate heater and air conditioner. This is likely to be a motivating factor in the rise of heat pumps for cooling.

Figure 3: Cooling Equipment Shipments, 2012-Q3 2025

Amid all of this, the One Big Beautiful Bill Act eliminated the Energy Efficient Home Improvement Credit and the Residential Clean Energy Tax Credit at the end of the year. The law also sets the New Energy Efficient Home Tax Credit, the Low-Income Communities Bonus Credit Program, and the Energy Efficient Commercial Buildings Deduction to end in 2026. These could represent big setbacks for building electrification, as they take away opportunities for building owners and contractors to make electrification more affordable. In fact, the anticipated end of these credits may have driven higher shipments to take advantage of the credits before they expired. As AHRI releases data through the end of 2025 and into 2026, we’ll see whether this effect played out as the credits were sunset.

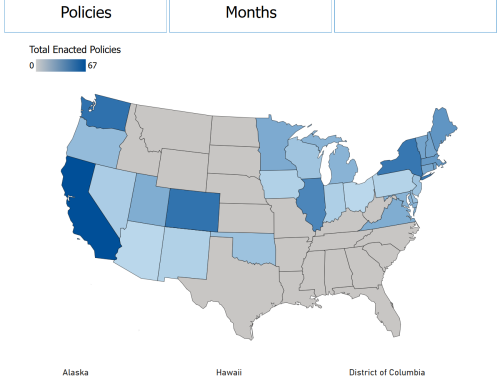

Thirteen states offer federally funded rebates for home electrification

Also in 2025, the Buildings Hub launched the Home Energy Rebates Tracker, which kept tabs on the Home Energy Rebates programs supported by the U.S. Department of Energy and administered by states to help Americans afford energy efficient and/or electric home upgrades. In the beginning of the year, facing uncertainty around the continuation of federal funding, Arizona, California, Colorado, and Rhode Island temporarily paused their programs. By the end of the year, once some of the uncertainty was settled, 12 states and DC offered rebates for appliances and six of those also offered rebates for whole-home projects (Figure 4). The only new programs to open in 2025 were Indiana’s Home Efficiency Rebate and Home Appliance Rebate programs and Michigan’s Home Energy Rebates programs. The remaining programs are still awaiting signed contracts from the U.S. Department of Energy. Although neither the states nor the federal government has provided many public updates about this process, some states are moving ahead with preparing their programs regardless. Most recently, South Carolina reportedly was set to award operator contracts for its Home Energy Rebates programs in mid-January.

Figure 4: Status of Home Energy Rebate programs in January 2026

Although most states do not provide public information on the status of their funding, California has kept homeowners informed as its programs have seen major interest. As of January 7, 2026, the single-family appliance rebates were fully reserved in Central and Southern California and were expected to run out in Northern California by the end of the month. It is currently unclear whether additional funds will be made available in the future, as the future of the federal funding for these programs is unclear.

Thermal energy networks are heating up

States like Illinois, Maine, Texas, and Washington enacted new laws to explore or authorize the development of thermal energy networks to enable neighborhood scale decarbonization. Each state’s legislation took slightly different approaches to the issue. Illinois passed the Clean and Reliable Grid Act in October. Among other provisions, it authorized the state climate bank to create a Thermal Energy Network Revolving Loan and Financial Assistance Program to help capitalize projects in the state. In Maine, LD 1619 directed the governor’s office to issue a request for information to inform the potential creation of a thermal energy network program in the state. In Texas, HB 4370 amended the Local Government Code to explicitly allow geothermal water conveyance as a public improvement project, opening up opportunities for utilities to set up thermal energy networks with government support. Washington’s HB 1514 created a new class of “thermal energy company” in utility regulation to encourage the development of thermal energy networks. Thermal energy companies are afforded the same benefits as electric, gas, water, or wastewater utilities and must be allowed to sell thermal energy wholesale or retail.

Meanwhile, Massachusetts saw positive and negative developments around thermal energy networks. Eversource’s pilot in Framingham that went online in 2024 was reportedly proceeding well, while National Grid canceled its Lowell pilot due to high costs. But Massachusetts is far from the only state with a thermal energy network. In a Buildings Hub Live episode in November, Atlas spoke with experts about two different kinds of thermal energy networks in the Midwest: one serving a town in Iowa and one serving a corporate campus in Wisconsin. Both networks have seen success and enthusiasm from their users and a lot of interest from other places looking to replicate their successes.

State efforts to address affordability and electrification with less federal support will define 2026

Despite federal headwinds, states and localities are surging ahead on building electrification, saving money and emissions while they’re at it. Heat pumps are continuing to outsell gas furnaces, but will this trend continue with the end of federal tax credits? Cities are adopting creative solutions like thermal energy networks to fit their unique needs and combat rising electricity prices, but will the projects get built? How will rising electricity prices affect the economics of switching from fossil fuels to high-efficiency electric appliances for space and water heating? As we continue into 2026, Atlas will continue to keep an eye on key trends like fuel prices and state policies on building electrification and will roll out new features to keep the community informed on all the latest developments.